Believe it or not, medical bills arise by 8 percent every year, along with other common and essential treatments for serious ailments such as stroke, diabetes, cancer, and many others. Our country’s health expenses attained almost ₱700 billion way back in 2017, and are still continuously inflating up until now.

Of this amount, more than ₱300 billion came from the patients’ pockets.

With this highly noticeable amount, maybe you are curious as to why a dozen lots of citizens aren’t inclined nor aware of health insurance and its loads of benefits. Unfortunately, various factors such as lack of knowledge regarding it exist.

But first, what Is Health Insurance?

Health insurance is typically collateral that aids you in paying hospital bills (either medical or surgical), dental expenses, and expenditures on prescribed drugs. It is more like a system that finances and reimburses your health expenses through your contributions or paid taxes in an insurance policy.

It can grant you the part or maybe full payment for your medical costs since it can cover a wide range of medical services.

Moreover, if you have no choice but to leave work because you are sick (disability leave), or if you need to temporarily take a leave to take care of your daughter, son, or baby (parental leave), health insurance can provide you income benefits despite your situation.

Several companies also include health insurance benefits to attract good quality workers. Sometimes, the employer covers the premium costs, but most of the time, it is recompensated through the employee’s paychecks.

If your health insurance is arranged and managed by a private agency or an insurance company, it is called Private or Voluntary Health Insurance. Of course, there is a contract of agreement that ensures the specific sustenance you can get from your health insurance.

This private health insurance is commonly funded by certain groups of employees whose payments may be sponsored by their employers. Despite that, there are also other plans specified for individual policies.

On the other hand, if the health insurance you obtained is from the specific provisions sustained by your taxes or legal compulsory contributions, it is called Government or Social Insurance. This kind of insurance emerged worldwide when the German government commenced a program based on the paid contributions of employees and employers in different industries in 1883. Truth be told, some governments still finance private insurance programs, resulting in a vague difference between private and public programs.

How does a Health Insurance Plan Work in the Philippines?

Managing health insurance can sometimes be complicated since many managed care plans such as POS and HMOs demand you to receive care and assistance from a certain healthcare provider to obtain the highest level of insurance coverage.

These managed care plans let you select your primary care physician who monitors you, renders recommendations about treatments, and refers you to other medical specialists designated to your health condition. On the contrary, there are also PPOs who have lower charges for using a primary care physician, however, you should not expect them to refer you to other medical specialists.

If you refused to accept care from healthcare providers, there are instances when your insurance company may turn down payments for your fees, especially if you obtained it out of their network. This is a huge disadvantage in your place since seeking care outside your insurance company’s network will make you pay a higher amount and you won’t get any benefits.

In addition, they may also refuse to cover fees for certain services that you got without authorization, and they may also reject the payment for branded drugs, especially if there is a comparable medication or generic version of it in the market, and at a lower cost at that.

When you come across this situation, you do not need to complain because all of these rules are mentioned in the material copy that your insurance company has given you. Thus, it is always worth checking.

Health insurances also deductibles, which you need to pay before your health insurance covers your claim. It also has co-pays or co-payments, which is a standard for every insurance company. You need to pay this fee to acquire services such as prescription drugs and doctor visits.

Moreover, it also has co-insurance which you are required to pay, despite reaching your deductible amount. Technically speaking, the higher premium you apply, the lower your deductibles will be.

So, it is better to always compare and weigh the benefits of lower monthly insurance costs with large expenses than higher monthly insurance costs with low expenses in case of a major accident or ailment.

Aside from health insurance, qualified ill people can also get disability insurance, LTC insurance, and critical illness insurance to get a hold of supplementary medications in the market.

6 Importance of Having A Health Insurance

Having accessible health insurance to cover your and your family’s medical expenses is truly beneficial, especially during emergency situations. Aside from the financial help, it can give, it can also aid in defying inflation on various medical treatments.

Health insurance makes life more convenient to you and here are some of the justifications why you should consider getting one now.

1. Protection for your family

Apparently, you can select a health insurance plan which covers your entire family with a single policy rather than getting separate ones. It is convenient since you need not worry anymore if something happens to your elders or younger kids since it assures you that they will get the best medical treatment out there.

If you want to apply for one, you should talk to experts so that you won’t get a biased opinion. Therefore, you can choose what is best for your family.

2. Sufficient coverage of insurance

Truth be told, some workers already have health insurance especially if it is provided by their employers. However, there are instances when the amount inside your health insurance is not enough to cover your medical expenses, which is exactly why you should always check it.

As time goes by, medical treatments inflate, but if you cannot currently avail for higher coverage of insurance plan, it’s definitely fine since you can start with a low amount then continuously increase it through the following years.

3. Resistance to lifestyle diseases

Nowadays, lifestyle diseases such as diabetes, heart ailments, respiratory problems, obesity, and many others appear on anyone, no matter what their age is. Some of the factors that contribute to it are addiction, stress, unhealthy eating habits, and a sedentary lifestyle.

If you get health insurance now and started investing in it, you do not have to trouble yourself in getting lifestyle diseases since it can support you financially and make you able to have regular medical tests to detect any illness as soon as possible.

4. Confronting medical inflation

Realistically speaking, medical costs increase along with the advancement of technology and further developments of diseases. Unfortunately, the fees for room rent, ambulance charges, operations, diagnosis tests, surgeries, doctor’s consultation, and medicines also increase with due time.

In that sense, having available health insurance may come in handy especially if you are not prepared for such expenses. Thus, the burden of cost will not trouble you.

5. Additional savings

In case of an emergency situation or accident, you need not trouble yourself with medical expenses since health insurance can cover them. Lesser stress, lesser expenses. Therefore, you can save up more for your intended future plans such as outings with the family, buying a home, educational expenses for your children, and your own retirement.

Besides, having health insurance makes you able to avail yourself of tax benefits.

6.Earlier security

If you get health insurance while you are still young and healthy, you can avail of plans with lower rates and as time goes by, the advantages you will receive will grow along with your age.

In addition to that, more extensive coverage options will be offered to which you will find useful in life if you once you are older and you got sick.

Types of Health Insurance in the Philippines

There are different ways to avail of health insurance, it is always better to have this kind of financial support when it is most needed. In the Philippines, these three are the most recommended health insurance:

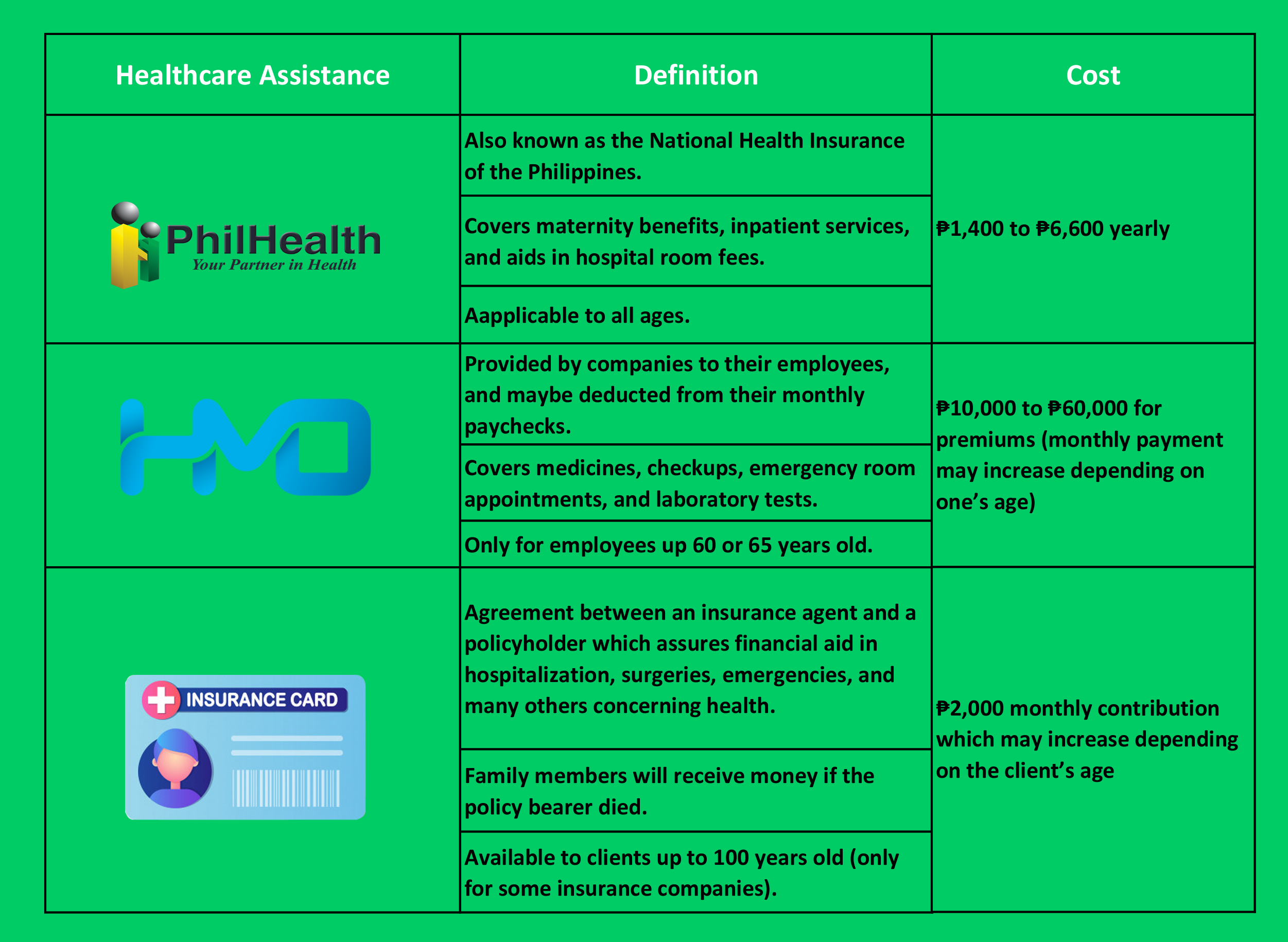

1. PhilHealth

PhilHealth is health insurance supported by the Philippine government. It is accessible for every Filipino because of its cheap monthly payment. This insurance provides financial assistance to all citizens who need medical assistance. Membership is voluntary whether employed or unemployed but if you’re an employee, half of your monthly contribution will be paid by the employer, and the other half is deducted from your salary.

PhilHealth covers a portion or even as much as 100% coverage of hospital bills depending on the member’s eligibility. This health insurance still has limitations, they cannot cover all of your medical expenses if your illness requires long-term or expensive treatments. On the other hand, you can pay bigger than your selected premium this will help you add benefits to your PhilHealth package.

2. Health Maintenance Organization (HMO)

HMO Health Insurance is commonly given by private companies to their employees. An individual HMO plan is better than those of the workers because an employee’s plan is chosen by their company. An individual member can adjust their plan based on their healthcare needs.

On the other hand, being an individual member is somehow expensive. This health insurance can provide enough sum of assistance that you won’t even need to pay any cash for an inpatient or outpatient service such as admission and room expense, laboratory expense, and doctor fees.

3. Health insurance plan

Many private companies offer a health insurance plan. Although these plans may quite cost a lot, it’s surely worth it because these plans tend to provide enough assistance so you won’t worry about your medical expenses.

Think wisely before getting a health insurance plan. You’ll need to know a lot about yourself and your family history because you’ll need to choose what kind of package you’ll need in the future. It is much better if you get insurance as young as you can so you’ll get to save a big sum of amount to your insurance.

In the Philippines, What is the Average Cost of Health Insurance?

Health Insurance comes with a price. Don’t hesitate to invest money for your health insurance because it will surely serve its purpose in time.

Starting from the most affordable insurance, there is PhilHealth. You can avail of their insurance for a minimum of ₱1,400 to ₱6,600 a year.

HMO plans differ depending on your selected package. Their health insurance varies from around ₱10,000 to ₱60,000 annually.

Like any other insurance, private health insurance varies depending on your premium. In the Philippines, the lowest health insurance plan that you can get would cost you around ₱40,000 annually.

3 Things to Remember When Looking for A Health Care Insurance Provider

1. Health Insurance Policy

Health insurance policies are the first thing to consider. This indicates the price and coverage of each premium that a person can avail of. Look for the package that you can benefit from the most based on your health and your family’s health history. If you chose a cheaper package, the benefits are expected to be minimal, it might just consume a portion of your medical expenses.

However, if you choose a more expensive premium, it can pay for all of your hospital bills that you’ll only have to worry about resting and recovering.

The health insurance policy can be updated by the provider. They can add more benefits to your chosen package which is a very good thing for you.

2. Provider’s connections

The medical insurance coverage also varies on the insurer’s affiliates. They only provide medical care that can be accompanied by doctors or hospitals under their contract. It is much better if your health insurance provider has a lot of accredited doctors and hospitals so you would have other choices when you need more consultation for your disease.

3. Health insurance’s accommodation

Some health insurance providers offer either inpatient or outpatient care only and sometimes both. It is an advantage if you choose the health insurance that offers both inpatient and outpatient care. Inpatient services include hospitalizations and medicines that means if your condition doesn’t require you to be hospitalized, your expenses won’t be covered by the insurer.

That is why you should include outpatient services when choosing medical insurance. Outpatient services provide you laboratory tests and physical examinations.

You can go to the hospital and get medication without getting admitted to the hospital and the expenses will be covered by your health insurance.

Best Health Insurance Companies in the Philippines

| Company | Founded |

| Sun Life Philippines | 1865 |

| AXA Philippines Inc. | 1816 |

| BPI-Philam | 1933 |

| Pru Life U.K. | 1848 |

| FWD Philippines | 2013 |

| Kaiser International Group, Inc. | 1945 |

| Caritas Health Shield | 1995 |

| Manulife Philippines | 1901 |

| MediCard | 1986 |

| Maxicare Health Corporation | 1987 |

As the year passes by, the medical and health expenditures are uprising by 8 percent wherein according to FY 2019 DOH National Expenditure Program Report, from the PHP 381 billion in 2010, it has already reached 684 billion for 2017 and still rising.

With this scenario, Filipino patients have been paying PHP 373 billion out of their pockets just for the year 2017.

That is why understanding the idea of what and how does health insurance is really important as above stated which can save you from several expenses when it comes to financial assistance for services like laboratory tests and medication, surgery and especially it is an aid for the costs of medical check-ups and treatment once you were out of cash.

Company Summary

If your mind was thinking about having health insurance, this article will provide you the 10 best and affordable health insurance companies in the Philippines and ways how can get coverage as well:

1. Sun Life Philippines

Sun Life Financial Inc. is a financial services company in the world that was founded in Canadian Matthew Hamilton Gault in 1865. Nowadays Sun Life was one of the largest financial services companies together as being the oldest in the world.

![]()

- Offers SUN Fit and Well, SUN Senior Care, SUN Cancer Care, SUN LifeAssure, SUN Healthier Life, Sun First Aid, and Sun Maiden, and Sun Maiden Plus

- SUN Fit and Well is a life and health insurance that endows life insurance benefits and covers you from 100 critical illnesses until the age of 100.

- SUN Senior Care provides you 150% financial benefit that is equal to the plan’s face amount if you were diagnosed with any of the 17 advance-age critical illnesses conditions they covered.

- SUN Cancer Care provides cash benefits for the covered early and late stage of cancer conditions, aside from this, they will also give a one-time cash benefit if you will undergo surgery due to a covered benign tumor.

- SUN LifeAssure assures your family protection against any of the critical conditions.

- SUN Healthier Life provides protection and financial help for you to recover in any stage of critical illnesses.

- Sun First Aid provides financial benefits not only for hospitalization or surgery but also for uncertain events like accidents, disability, etc.

- Sun Maiden and Sun Maiden Plus are specifically designed f for women. It provides life insurance coverage and female critical illness benefit plus the maternity benefits (only for Sun Maiden Plus) that will assist the up to three children delivered and in case of any complications during pregnancy.

| Website: | www.prulifeuk.com.ph |

| Customer Care: | (632) 8683 9000 (632) 8884 8484 |

| Email address: | contact.us@prulifeuk.com.ph |

| Address: | 9/F Uptown Place Tower 1, 1 East 11th Drive, Uptown Bonifacio, 1634 Taguig City, Philippines |

2. AXA Philippines Inc.

Axa S.A or AXA is a French multinational insurance firm in Paris since 1816 (204 years ago). AXA is not an acronym but it was picked to be the name of the company because it is easy to pronounce by people who speak in any language.

AXA Philippines is a joint venture between the AXA Group, one of the world’s largest insurance groups, and the GT Capital/Metrobank Group, one of the Philippines’ largest diversified conglomerates.

- offers Critical Illness Coverage (Health Start, Health MaX, Health eXentials) and Global Health Access

- Health Start is an insurance plan that covers support for critical health conditions of the family especially the child, life insurance coverage, and even return of premium at the age of 75 with less any benefit or support paid.

- Health Max is a lifetime Health Coverage that even when your HMO expired, lasts until the age of 100!

- Health eXentials doesn’t require any medical examinations. The good thing here is you can have full control of spending as you deem it fit, wherein guaranteed cash packages or benefits comes into three options; Starter, Advance, and the Deluxe.

- Global Health Access gives you world-class medical and health coverage wherever inside and outside the Philippines with 27/7 support and hassles free and cashless transactions.

| Website: | www.axa.com.ph |

| Customer Care: | (+632) 8 5815-292 (+63) 917 1709292 (Globe) (+63) 998 5889292 (Smart) |

| Address: | 34th Floor GT Tower, Ayala Ave. corner H.V. Dela Costa, Makati City, Philippines |

3. BPI-Philam

The BPI-Philam Life Assurance Corporation or BPI-Philam alliance has started in 1935 and focuses on Asia- Pacific region.

![]()

- Offers you 5 choices: Critical Care 100, Critical Max Care, Critical Care Plus, Health Save 10, and Life Health Protect

- Critical Care 100 is a life and health insurance plan that grants an issue from age zero to 100 protecting you from 100 covered critical illnesses with your family. And if you are such a healthy human, it could also make your pocket healthy as you can gain rewards and discounts from its partners.

- Critical Max Care and Critical Care Plus aids financial help in the early stages of a critical illness and recovering and even accidents. It also includes the Philam Vitality Rewards wherein you can enjoy an upfront additional coverage of 20% within the policy and any add-ons attached.

- Health Save 10 is a 10-year health plan that aids financial benefits and assistance for hospitalization and gets your money back at the end of the said plan if the policy is still active and the number of days accumulation cash benefit on the hospital has been paid not exceeding to 365 days.

- Life Health Protect is a health plan that longs for 10 years that supports you from health setbacks by receiving a cash benefit for the diagnosis of critical and even terminal illnesses.

| Website: | www.bpi-philam.com |

| Customer Care: | (632) 8 5285501 1-800-188-89100 (Toll-Free) |

| Address: | 15th Floor BPI-Philam Life Makati, Ayala Avenue, Makati City 1226 |

4. Pru Life U.K.

Pru Life UK is a 1996 branch of the British financial services giant Prudential plc that has more than 170-year legacy worldwide. In 2019, Pru Life UK ranked 2nd based on the Insurance Commission in terms of total premium income and new business annual premium equivalent.

![]()

The Pru Life UK local headquarter is located in Uptown Bonifacio, Taguig City.

- Offers PRULink Assurance Account Plus, PRU Life Care Series for Critical Illness, PRUShield, PRUWellness, and PRU Personal Accident

- PRULink Assurance Account Plus is designed for people who want a comprehensive life and assured insurance protection that provides critical illness, life, and death protection by investment components and protection.

- PRU Life Care Series for Critical Illness is annual renewable term products until the age of 70 that aids cash benefits to cover the expenditures of your treatments for your critical illness depending on what Life Care you have such as Life Care Plus, Life Care Advance Plus, and Multiple Life Care Plus.

- PRUShield is an annual renewable term product until the age of 65 that provides daily hospital income benefit wherein it comes with daily cash benefits up to 365 days in able to aid your recovery due to an accident, injury, illnesses and you can also get a death that pays a lump sum amount.

- PRUWellness is also an annual renewable term product until the age of 65 that provides you a lump and daily cash benefits for your hospitalization.

- PRU Personal Accident is an annually renewable plan that will cover your injury or even death due to an accident. It has various packages available to suit your age, lifestyle, income, and occupation.

| Website: | www.valucarehealth.com |

| Customer Care: | (02) 8702-3388 / 5317-4388 |

| Email address: | wecare@valuecarehealth.com |

| Address: | #33 Meralco Ave. Brgy. San Antonio Pasig City |

5. FWD Philippines

FWD is an insurance business of the Pacific Century Group that was established in 2013 in Asia. Take note that FWD has nothing to do with the acronym.

![]()

- an insurance business of the Pacific Century Group that was established in 2013 in Asia

- Offers Critical Illness Insurance and Cancer Insurance

- Critical Illness Insurance is set for health purposes that will surely cover you from up to three claims against the 42 major critical illnesses they cover. And once you’ve been diagnosed with one of the major illnesses covered, they’ll waive you a future premium payment so you don’t need to worry about the payments during recovery and let you give ease to focus on your well-being.

- Cancer Insurance provides you financial protection up to ₱2 million for up to 15 years, which you can pay for as low as PHP 6, 000 for five to 10 years annually to lessen your worries about winning the fight.

Address:19F W Fifth Avenue Building, 5th Avenue corner 32nd Street, Bonifacio Global City, Taguig City 1634

| Website: | www.fwd.com.ph |

| Customer Care: | +632 8888 8388 |

| Email address: | customerconnect.ph@fwd.com |

5. Kaiser International Group, Inc.

Kaiser International Group, Inc. is a health care provider that was founded by Filipino professionals in 2004. Unlike others, Kaiser is an HMO company that has geared products with a long-term duration of health and medical needs of people especially whose already out of the job and retired.

![]()

- offers plans like Long Term Care and Short Term Care and even a Senior Care Plan

- Long Term Care offers insurance benefits like term life insurance, basic medical benefits, accredited hospitals, and even doctors and specialists, accidental death, and dismemberment insurance.

- Short Term Care includes various perks Preventive Health Care, in and Out-Patient Care, Dental Care, and Emergency Care.

- Senior Care Plan is a specialized plan for people ages 61 and above wherein the comprehensive range of maximum Medical-Healthcare Benefits is limited to PHP 1,000,000.

| Website: | www.kaiserhealthgroup.com |

| Customer Care: | (02) 892 9634 |

| Email address: | support@kaiserhealthgroup.com |

| Address: | Ground Floor King’s Court I Building, 2129 Don Chino Roces Avenue Makati City |

6. Caritas Health Shield

Caritas Health Shield has revolutionized the concept of health care services in the country since its establishment in 1995 with our superior and iconic multi-year health plans.

![]()

The best customer-friendly medical services from our accredited nationwide network of over 13,000 doctors of medicine in varied fields of specialization, dentists, hospitals, laboratories, and diagnostic clinics.

| Website: | caritashealthshield.com.ph |

| Customer Care: | 0917 – 305 5152 0945 – 369 4180 0945 – 368 7305 0956 – 089 5230 0945 – 369 3891 0945 – 369 4120 0945 – 369 3942 0945 – 369 4140 0945 – 369 3945 |

| Email address: | wecare@valuecarehealth.com |

| Address: | 97 E. Rodriguez Sr. Avenue, Quezon City |

8. Manulife Philippines

It is a financial corporation (formerly known as The Manufacturers Life Insurance Company) established in Canada in 1887 that provides multinational insurance services. Moreover, it is the largest insurance company in Canada and gained 28th place for the largest fund manager in the world.

![]()

Manulife Philippines offers affordable health insurance wherein you can choose your plan based on three options they provided for the clients; Adam, Eve, and the Healthy Choice.

- Offers affordable health insurance wherein you can choose your plan based on three options they provided for the clients; Adam, Eve, and the Health Choice

- Adam is a comprehensive health plan that was made specifically for men. It provides help and support for the expenses of the said man once he was diagnosed with cancer wherein Manulife will support you by annual cash for three consecutive years in able to get your treatments for your fight.

- Eve plan is exclusive for women. Just like Adam, it also provides the same kind of aid for its owner who’s fighting against cancer, financial support for the loved ones, and the same percentage of face amount to receive once you were diagnosed with any 60 critical illnesses they covered.

- Health Choice lets the owner enjoy critical illness coverage, hospital benefits, emergency, and life insurance in one plan. Once you’ve diagnosed with any 60 illnesses they cover, Manulife will give you financial aid for the treatments you need. Aside from this, they also help you in your hospitalization by daily cash support up to the year of confinement.

If you are thinking to get your one, you can talk to their financial advisor via online:

| Website: | www.manulife.com.ph |

| Customer Care: | +632 8884 7000 |

| Email address: | phcustomercare@manulife.com |

| Address: | 10th Floor NEX Tower, 6786 Ayala Avenue, Makati City, 1229 |

9. MediCard

MediCard Philippine Inc. was incorporated in 1986 and formally founded and 1987. It is the leading HMO in the Philippines that was managed by doctors to “provide comprehensive healthcare protection to individuals of Metro Manila as well as in key provincial areas.

![]()

MediCard has divided their offered plans based on the primary customer needs for

“Myself,” “My Family,” “My Employees,” “Senior Citizens,” “Maternity and Pre-Existing Conditions” and OFWs with beneficiaries in the Philippines.”

Here are the following plans for each category wherein you can visit their website link below for the specific details and ventures:

For Myself

- Heath Check (Link)

- HealthPlus(Link)

- RxER (Link)

- My MediCard (Link)

- Individual And Family (Link)

- VIP (Link)

- Medicard Select (Link)

For My Family

For My Employees

- MediCard Select (Link)

For Senior Citizens

For Maternity and Pre-Existing Conditions

- MediCard Select (Link)

For OFWs with beneficiaries in the Philippines

| Website: | www.medicardphils.com |

| Customer Care: | Hotline (02) 8841-8080 Toll Free Numbers 1-800-1-888-9001 (PLDT & Smart) 1-800-1-994-8400 (Globe & Touch Mobile) |

| Email address: | contact.us@prulifeuk.com.ph |

| Address: | 8/F The World Ctr., 330 Sen. Gil J. Puyat Ave., Makati City |

10. Maxicare Health Corporation

In 1987, Maxicare Health Corporation was established together as one of the pioneers of the HMO industry and remains one of the top health insurance companies.

It was established by a group of doctors and businessmen with the vision of delivering a better healthcare system.

- offers MyMaxicare, MyMaxicare Lite, EReady, Eready Advance, Maxicare PRIMA

- MyMaxicare is a program created for an individual or family that has several payment options to pay based on what fits on your budget. It includes and Out-Patient Care, Emergency Care, Dental Care, etc.

- MyMaxicare Lite is a one-time availing In-patient prepaid card that covers eight illnesses such as Chikungunya, Cholera, Dengue, Gastroenteritis, Leptospirosis Malaria, Paratyphoid, and Pneumonia and thyroid for the age of 2 and 60.

- If an emergency comes in bad timing, you can avail EReady and Eready Advance, while if you want some premium benefits, you might need Maxicare PRIMA. Maxicare PRIMA endows 255 types of lab and diagnostic tests within the hospital that cover Maxicare. In addition, it also grants unlimited Outpatient Consultations.

| Website: | www.maxicare.com.ph |

| Customer Care: | + 632 8582 1900 (PLDT) + 632 7798 7777 (GLOBE) |

| Email address: | customercare@maxicare.com.ph |

| Address: | 8/F The World Ctr., 330 Sen. Gil J. Puyat Ave., Makati City |

Global Health Insurance Plans for Expats and Foreigners in the Philippines

The Philippines truly has a lot to offer for foreigners and health insurance is not an exemption. Persons who work out of their home country are also given a chance to avail expatriate health insurances to make sure that they are secured wherever they go.

The Philippine government allows expatriates to have PhilHealth insurance and like any other employee in the country, half of the premium is deducted from the employer, and the other half is deducted from the employee’s salary.

Even self-employed or unemployed ex-pats can enroll in PhilHealth as long as they have legal residency status.

Expatriates can avail of international medical insurance which may cost quite a lot but still considered affordable because foreign nationals earn just enough for it.

As an ex-pat, you should consider the geographic location of your workplace. Some of the places in the Philippines can’t offer a high-quality health care system because of the lack of doctors and hospitals in rural areas.

You need to make sure that your health insurance provider offers medical evacuation if you work in a rural area.

Some Scenarios When A Private Health Insurance is Needed

There are instances when you will be required to get health insurance, whether you like it or not. They are as follows:

- If you are unemployed – Even if you lose your job, you can still continue your health insurance by means of your employer’s health insurance plan. There is a program called the Consolidated Omnibus Budget Reconciliation Act (COBRA), which authorizes employees to do such a thing despite losing jobs or decreased working hours. In this program, your employer pays a partial amount of your healthcare premium on your behalf, that’s why applying for it costs high since you, yourself, need to pay for its entire fee after your employer did his/her part.

- If you reached age 26 or older – As stated in the Affordable Care Act (ACA), young people, especially teenagers, are included in their parents’ health insurance policy but that is only until they turn 26 years of age. Henceforth, they must provide their own insurance policy and stop depending on their parents.

- If you are a part-time employee – Since part-time jobs do not offer you health benefits such as insurance, you need to get your own so that you won’t have trouble with financing yourself the moment an unexpected accident happened to you.

- If you are a business owner and you have employees – Companies offering health benefits to their employees is the common thing nowadays, that is why you should offer one, too, if you are planning to start a business. It attracts workers and in that particular sense, you must purchase a business health insurance plan.

- If you are self-employed – This situation is almost the same as the part-timers since they both work for themselves and no one but them will provide their health insurance. Therefore, it is better to get one as early as possible. It can be beneficial to you in many ways.

If you retire – You will no longer be a beneficiary of the COBRA program the moment you retire. You can apply for Medicare the moment you turn 65 and you can also avail of individual private health insurance.

Take note that this is only for a certain individual, thus, if your family members are covered in your previous insurance plan, they might need to apply for their own now.

10 Things You Need to Know Regarding Life Insurance

Here are 10 things that you need to know about life insurance:

- If you’re supporting someone’s financial needs, you need life insurance to avoid adding too much to their expenses.

- Life insurance helps those left behind in dealing with the unexpected financial consequences due to loss of life.

- Life insurance is a contract between the life insurance company and the beneficiary. The policy owner pays the company and the company pays the life insurance claim receiver after the death of the owner.

- Life insurance works around four persons. First is the insurer or the life insurance company. The owner or the person who availed the life insurance. The insured is the person who is expected to receive insurance. And lastly is the beneficiary or the one who will receive the life insurance claim after the insurer passes away.

- Having life insurance doesn’t mean you are ready to die, you are just preparing compensation for those who’ll be left behind.

- There are life insurances that only last for a few decades, even if you paid a lot for it, if your term has ended and you’re still alive, you’ll get nothing out of it. There are different kinds of life insurance, don’t rush in choosing and think wisely before getting one.

- Some people considered life insurance as an affordable plan but it can get extremely expensive if you’re into smoking or you have health problems.

- You can change the coverage of your life insurance if you suddenly have other factors to consider that might affect your life span, but it might cost you a sum of amount.

- Life insurance is generally tax-free but some beneficiaries are asked to pay some taxes. Read the policy carefully before enrolling in insurance to avoid such circumstances.

- Some life insurance policies allow you to have living benefits. You can have a sum of amount even if you’re still alive.

The Best Private Hospitals in Manila

1. The Medical City

The Medical City (TMC) is located in Pasig City, Metro Manila. It offers high-quality medical care for inpatient and outpatient services. Their world-class facility can serve more than 400,000 patients a year.

They have been accredited by Joint Commission International Accreditation (JCIA) because of obtaining the highest standard of quality for healthcare organizations internationally. They are commended for their best access to care, patient safety, and continuity of care to patients.

TMC has experts in Medicine, Surgery, Orthopedics, Obstetrics, Gynecology, Pediatrics, Ophthalmology, Otolaryngology, Anesthesiology, and Psychiatry. They can also offer the best services in Pathology, Radiology, Nuclear Medicine, Physical Medicine, Rehabilitation, Pain Management, Radiation Oncology, and Chemotherapy.

2. St. Luke’s Medical Center

According to the evaluation of the Diplomatic Council last 2014, they considered St. Luke’s Medical Center as the “Best Hospital of the World”. They are affiliated with international organizations that helped them have world-class medical services.

Their facilities are located in Quezon City and Global City, Taguig, and both facilities are leading as the most advanced hospitals around the world. They can provide service for around 60,000 inpatients and 2.7 million outpatients annually.

St. Luke’s Medical Center has advanced technologies that can offer a comprehensive approach to diagnosis and treatment. They have experts in various fields such as Medicine, Surgery, Gynecology, Pediatrics, Psychiatry, and many more.

3. Makati Medical Center

![]()

MakatiMed’s decades of medical innovation and compassionate care to its patients, their families, and community is enhanced by pioneering significant clinical research initiatives, commitment to continuous modern medical advancement, and training new generations of healthcare providers who can proudly continue its tradition of excellent healthcare service.

The hospital’s specialty society-accredited internship, residency, and subspecialty fellowship training programs have consistently produced many of the outstanding physicians of the country today.

10 Steps in Finding a Good Doctor in the Philippines

- Determine what kind of doctor you need. Doctors have specific expertise so you’ll need to know first the possible treatment that you’ll need based on your symptoms.

- List all the doctors (that is expert in the field that you need) around your area.

- Evaluate each doctor according to your preference and narrow down those who seem to not meet your expectations. You can evaluate them based on your preferred age, gender, and spoken language.

- Make a better background checking to your top choices. Consider their years of practice, license, and other patient reviews about them.

- After choosing the best doctor among your options, make an appointment.

- Pay attention to their hospital/clinic facilities and the staff’s approach towards the patients.

- Observe the doctor while asking questions about your diagnosis and possible treatments that you need to undergo.

- Evaluate the doctor according to your observations.

- If the first doctor didn’t meet your expectations or you have doubts about his skills, you can get a second opinion from the other doctors among your top choices.

- Give good doctors good online reviews.

Frequently Asked Questions on Health Insurance

1. How much is Health Insurance in the Philippines?

If you want to avail of PhilHealth’s insurance, it will cost you ₱1,400 to ₱6,600 a year. HMO’s insurance costs around ₱10,000 to ₱60,000 annually. There are lots of private health insurance in the Philippines and the cheapest one will probably cost around ₱40,000. The price always differs depending on the health insurance package.

2. What are the differences between Health Insurance, PhilHealth, and HMO?

3. What Is the Difference Between Life Insurance from Health Insurance?

Life insurance is a contract that is effective upon the death of the insured person while health insurance is a contract that insures the owner’s medical expenses. Life insurance and health insurance require their owner to pay a lump sum of money monthly, quarterly, or annually.

4. What Is Health Insurance Policy?

A health insurance policy is the plan that the member chose to have. It indicates the price and the benefits for the insured person. The health insurance policy indicates the terms and agreements between the insurer and the insured person.

5. Why is it necessary for me to have a Health Plan?

You might not need it now since you are healthy and young, but you’ll definitely see its usage and advantages the moment you developed a disease or got into an unexpected accident or emergency later in life. These things are inevitable and when that time comes, it’s always better to be prepared, at least, to have an accessible health insurance plan at hand.

6. How do insurance companies make money?

Insurances are expected to return the money that you paid them using your premium. Insurers often offer prices wherein the total money that you paid for the plan will be equivalent to the claim that you’ll get. They make a profit out of your money. The collected money that the insured person pays will be placed as an investment pool.

The money will be pulled out from that pool when the insured person claims their benefits.

The insurer’s profit comes from the interest and returns on the investment that is made using the premium’s money when it is in the investment pool.

7. What is the Health Insurance Marketplace?

A health insurance marketplace is where you, your family, or your business can meet diverse health insurance plans. You can also weigh the differences between them to see which one is more convenient and which one is not. Moreover, this is where your other concerns regarding health insurance will be answered. If you are interested, go to their site (Healthcare.gov).

8. What are the Four Main Types of Insurance?

The four main types of insurance are Life Insurance, which is designed to aid your family’s burden in case you died unexpectedly; Health Insurance, which covers your medical bills and other expenses related to your health; Disability Insurance, which ensures that you will get the best medical treatment in case you become disables; and lastly, Auto Insurance, which ensures that you will pay repairs in case you are responsible for an accident.

9. Can A Foreigner Get Health Insurance in the Philippines?

A foreigner can always get health insurance in the Philippines as long as they work there or they have legal residency status. Expatriates can get health insurance whether they are employed or self-employed. Several foreign nationals can avail health insurance in the Philippines because they are married to a Filipino.

10. Can You Trust the Philippines Healthcare System?

A local or foreign national can trust the Philippines ‘ healthcare system. The Philippines has both public and a lot of private healthcare facilities. Both public and private facilities offer a standardized healthcare system.

The service and medications are also quite affordable if you compare them to the price outside the country.

All in all, you can trust the Philippines ‘ healthcare system, but don’t forget to be careful.

11. How to Find A Family Physician?

Some doctors agree with discount rates because of some specific health insurance plan, you’ll need to know if your plan offers this benefit to save up money. Choose a physician that is an expert for family or general practice. You can also try to consider recommendations from the people you know, you might get the best physician from them.

12. Are checkups part of Health Insurance?

Fortunately, yes. Health insurance provides free medical checkups. However, many are not aware of it since they are afraid that it will further increase the premium rates. Despite that, you should still get a medical checkup every once in a while.

13. Why Is Health Insurance Needed in the Philippines?

The Philippines offer a universal healthcare coverage system also known as PhilHealth. It is organized by the Philippine government and it is mandatory to have. Everyday situations in life are always inevitable. It is always much better to have health insurance to lessen the expenses made by your health condition.

Medical insurance in the Philippines is quite cheap and affordable, you won’t have too much loss if you try to avail yourself.

14. Do the Philippines Have Good Healthcare?

The healthcare system in the Philippines is at its best and highest quality if you live in the capital of the country, Manila. The hospital and healthcare facilities there are more advanced and affordable.

However, the facilities in some rural areas of the country are not the same, they lack facilities in some provinces.

Key Takeaways

- Medical bills rise by 8 percent every year, along with other common and essential treatments for serious ailments such as stroke, diabetes, cancer, and many others.

- Health insurance is typically collateral that aids you in paying hospital bills (either medical or surgical), dental expenses, and expenditures on prescribed drugs.

- If your health insurance is arranged and managed by a private agency or an insurance company, it is called Private or Voluntary Health Insurance.

- If the health insurance you obtained is from the specific provisions sustained by your taxes or legal compulsory contributions, it is called Government or Social Insurance.

- There are instances when your insurance company may turn down payments for your fees.

- Having accessible health insurance to cover your and your family’s medical expenses is truly beneficial, especially during emergency situations.

- Health insurance has its own inclusions and exclusions. Be sure to discuss these with your insurance agent.

- There are inevitable instances when you might need to purchase private health insurance.

- Health insurance provides free medical checkups.

- Health insurance helps an insurer deal with medical expenses, it can cover a portion or even the whole hospital bills.

- Life insurance is a contract between the beneficiary and the insurance company. The insurance provider pays the beneficiary after the death of the insured person.

- The cheapest health insurance in the Philippines is PhilHealth and it is organized by the Philippine government.

- Expensive health insurance has more benefits than cheap one.

- Study the terms and policies of the insurance before getting one.

- Expatriates and foreign nationals can get health insurance in the Philippines.

- The Philippine Healthcare System can be trusted because the facilities there are made with the best quality.

- The Medical City and St. Luke’s Medical Center are the best private hospitals in the Philippines, they offer world-class facilities and services.

If you’re looking for a good physician, evaluate his expertise, experience, and skills first. You can get another opinion from other doctors if you don’t trust the first physician who examined you.

How about you, what’s your story? Share it in the comments.

{kind=link}